Pre-Approval

Requirements

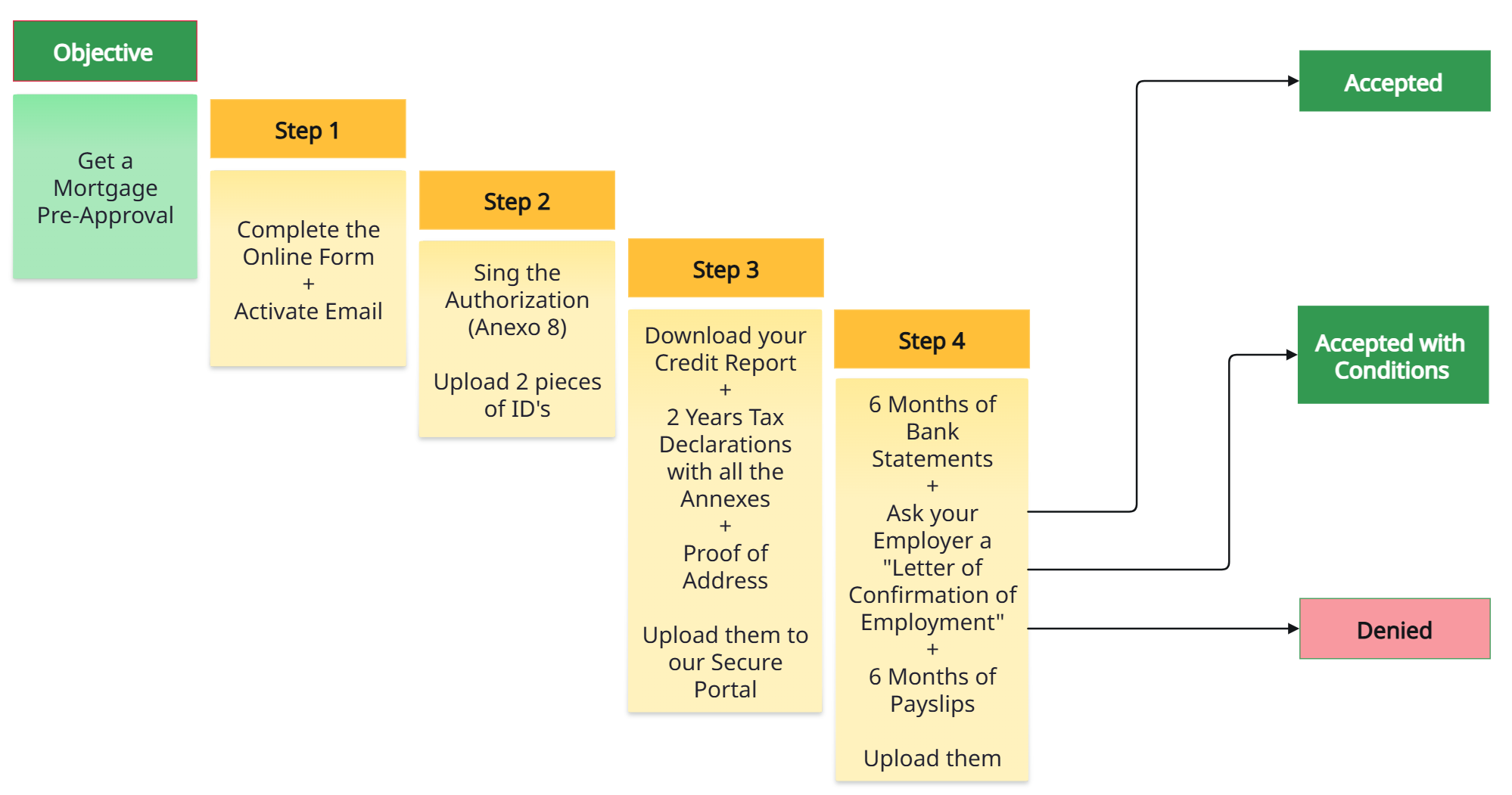

4 Steps "Pre-Approval Process"

Step 1

Book a Appointment & Complete the Online Form

Due to our High Volume demand, we didn't have choice but to charge

a 499$ USD fee for consulting.

(fully refundable at the funding of your financing at the Notary).

You'll find the answer to all your questions in the FAQ section below

Speak to you soon

Step 2

Sign the Authorization for us

to find you the best offer

We have an authorization form for you to sign.

It's called the "Anexo 8" and it's in spanish.

Don't worry, we got you cover with a traduction.

We need 2 Pieces of Valid ID's

with Picture

Passport

Drivers License

INE

Mexican Permanent Residency Card

Mexican Temporary Residency Card

*No need Mexican Residency to apply

Step 3

Credit Report

Go online and Download your Credit Report with Fico Score

2 Years of Tax Declarations

2023

W2 for all jobs (if more than 1)*

Form 1040 (Complete PDF)

Annex C*

2022

W2 for all jobs (if more than 1)*

Form 1040 (Complete PDF)

Annex C*

*In case of being a Self-Employed or Independant Worker,, please provide the Annex C

Proof of Address

We need the most recent one

to validate your Address in Canada.

No more than 60 days.

Electric Bill

Water Bill

Landline Phone Bill

Internet Bill

Step 4

Bank Statements

6 Months for Employee

12 Months for Independant

Letter of Confirmation of Employment

Ask to your employer to write you, a “Confirmation Letter of Employment” with:

The letter needs to be Dated and Signed

Company header (Logo & Complete Address)

Job title.

Job description.

Date of Hiring (dd-mm-yyyy)

Annual Income.

Social Security Number (or Employee ID#)

6 Months of Payslips

For Self-Employed or Independant Worker,

Please write in 1 page:

Description of your Work

Services you provide

and / or

List of Products you are selling

Can I refinance my existing property in Mexico with Prisma 67 ?

Absolutely. Refinancing with Prisma 67 allows you to adjust your mortgage terms to better suit your current financial situation, access cash for other investments or personal use, or consolidate higher-interest debts.

Our refinancing options are designed to help you maximize the value and equity of your property in Mexico.

We can offer you up to 85% of the actual Property value.

Who is eligible to apply for a mortgage with Prisma 67 ?

Prisma 67 specializes in mortgage services for foreigners, particularly Canadians, interested in buying or refinancing property in Mexico. Eligibility is open to both salaried individuals and self-employed professionals, regardless of whether they own property or have an existing mortgage in their home country. We also cater to those without a Mexican credit history.

Of cours, we also attend nationals clients.

What documents are required for the pre-approval process ?

To start the pre-approval process, you’ll need to provide the following:

2 pieces of Identification:

Valid passport or Driver's Licence,

Optional and not Necessary, Permanent or Temporary Mexican Residency

Proof of Income:

12 months pay stubs;

2 years tax returns, or financial statements if self-employed.

2 Years of NOA (Notice of Assessment for Canadian)

Letter of Employement signed by your Employer

Credit Report with Fico Score:

A credit report from your home country or a credit reference. The minimum score is 689.

Bank Statements:

Typically, the last twelve months of bank statements to verify financial stability.

Property Details:

Information on the property you wish to finance, including purchase agreements or construction plans. Additional documentation may be requested depending on the complexity of your financial profile or the type of loan.

Do I need to have a Mexican credit history to apply for a mortgage ?

No, you do not need a Mexican credit history to qualify for a mortgage with Prisma 67.

We understand that many of our clients are foreign nationals and instead consider your international credit history, financial standing, and other relevant factors to assess your eligibility.

How long does the pre-approval process take ?

Prisma 67 prides itself on an efficient pre-approval process. Once all necessary documentation has been submitted, pre-approval typically takes between 48 to 72 hours. This quick turnaround allows you to proceed with confidence in your property search or refinancing plans.

Is there a minimum down payment required to buy property in Mexico through Prisma 67 ?

The down payment requirements vary based on the type of mortgage and your financial profile.

Prisma 67 offers flexible down payment options, with some programs requiring as little as 10% down, depending on your eligibility and the property type. This makes it easier for you to enter the Mexican real estate market without significant upfront capital.

As a Foreigner, the Recommandable option is 25% or 30% cashdown

Why the interest rates seem higher in Mexico ?

There a lot of urban legends around the interest rate here in Mexico. At first sight it can looks high, but when you analyze completly, you'll find it very good and Logic.

Please don't get caught in the comparaison with your home-country. In Mexico, YES, the interest rate seems higher but it include a lot of things, it's not jus the interest on the loan, but the complete package of Insurances. Plus, here the financial products are taxable, so it includes 16% of IVA.

On the other hand, when you invest money with a bank they give you around 10% to 11% of returns. Here We are talking abouth the saving account, not on the stock market with the risk that's Involve.

What's included in the interest rate ?

Of course, the pure interest rate

Plus

A. Life Insurance;

B. Disability Insurance:

C. Reconstruction Cost Insurance in case of natural disaster

D. IVA (sale's taxes of 16%)

Is my Mortgage will appear on my home-country Credit Report ?

Absolutely not Mexican bank do not report your financing in your home-country.

Even your Mortgage Pre-Approval Process won't appear on your home-country Credit Report because you will go download by yourself, on Equifax (Canada) or Experian (USA), your Credit Report with Fico score and upload it on our Secure Portal.

You will just see personal check-up, did by yourself, but no mention of "Mexico"

Can I finance the purchase of land in Mexico through Prisma 67 ?

Yes, Prisma 67 offers financing options specifically for land purchases.

Whether you’re buying land as an investment, for future development, or to build your custom home, we provide the necessary funds to secure your plot. We also offer the flexibility to transition from land purchase to construction financing when you’re ready to build.

What's is the CAT that everybody is talking about ?

The CAT (Costo Anual Total), or Total Annual Cost in English, is a financial metric used in Mexico to represent the total cost of a loan or credit product. It is expressed as a percentage and includes not only the interest rate but also other costs associated with the loan, such as fees, commissions, and insurance.

The CAT provides a more comprehensive picture of the real cost of borrowing and is designed to help consumers compare different loan offers more easily. Here's a breakdown of what the CAT typically includes:

Interest Rate: The percentage charged on the loan amount over a period, usually expressed annually.

Commissions: Any fees charged by the lender for processing the loan or providing the service.

Insurance Costs: Some loans require life or property insurance, which is also factored into the CAT.

Other Fees: This might include administrative fees, fees for late payments, or any other costs associated with the loan.

The CAT is mandatory for all financial institutions in Mexico to disclose, making it easier for consumers to understand and compare the true cost of different credit products.

What is the average interest rate on a Mortgage in Mexico ?

Here's the real Truth with all included, not the "Announced" interest rates from the banks before they add up all the complete spices, here Prisma 67 is proud to give you the bottom numbers, no surprises or hidden fees at the end.

More or Less 13% to 15%.

Remember that the interest rate include:

Interest rate;

Life Insurance;

Disability Insurance,

Loss job Insurance for 6 months;

Reconstruction Cost & Replacement of Furniture in case of Natural Disaster;

IVA that adds itself on top of all the included accessories.

Here, Prisma 67 is giving you the REAL CAT (the Real TOTAL ANNUAL COST)

Please note that the value of your property normally double in 5 years. That's a fact to take in consideration when you will compare the Mexican interest rate with your home-country interest rate.

What is the process for buying a presale property in Mexico ?

Purchasing a presale property involves several steps, and Prisma 67 is here to guide you through each one:

Pre-Approval: First, obtain pre-approval to understand your budget and financing options.

Property Selection: Choose your desired presale property from a developer.Purchase Agreement: Sign a purchase agreement detailing the terms of sale and payment schedules.

Financing: We provide staged financing aligned with the construction milestones of the property(Applicable for houses and villas only), ensuring funds are released as each phase is completed.

In the case of Condo's Building, the banks won't get involved until the Completion of all the building and the obtention of the "Regimen of Condominio". This is for experts who are not in their first transaction in Mexico.

Not recommanded for first time buyer.

Completion: Once construction is complete, we finalize the mortgage and help you transition to property ownership. We work closely with developers to ensure a seamless process from start to finish.

Please note that in case of Presale, the Pre-Approval is valid for 12 months and before passing at the Notary, we will ask a new Credit Report with Fico score to verify if you kept good financial habits in your home-country.

How do I start the mortgage application process with Prisma 67 ?

To begin your mortgage application, simply schedule an appointment through our automated system on our website.

During this initial consultation, we’ll discuss your needs, explain our services, and guide you on how to submit the necessary documentation via our secure client portal.

Our team is available to assist you every step of the way, ensuring a smooth and stress-free application process.

We will be with you from the beginning to the signature at the Notary (Notaria Publica)

What are the benefits of using Prisma 67 compared to other mortgage providers ?

Prisma 67 offers several unique benefits:

Specialization in Foreigners: We understand the specific needs and challenges faced by foreigners investing in Mexico.

One of our Senior Broker, Alain Bessette, is the first and only Canadian to have his Mexican Mortgage Broker Licence in all Mexico. He worked in that industry for several years in Canada, so that gives Prisma a big advantage by understanding the foreign investors.

Quick Pre-Approval: Our efficient pre-approval process helps you move forward quickly with your property plans.

24/7 Customer Support: Our AI Assistant, Maria, provides round-the-clock support, answering your questions and guiding you through the process.

Flexible Financing Solutions: We offer customized mortgage solutions that cater to your individual circumstances, including flexible down payments and financing for a wide range of property types.

Comprehensive Support: From pre-approval to closing, we offer end-to-end support, ensuring a seamless and hassle-free experience.

Are there any additional fees associated with obtaining a mortgage through Prisma 67 ?

Yes, there are standard processing fees associated with obtaining a mortgage. These include appraisal fees and closing costs.

When the property is in a "Restricted Area" for example within 50km form the ocean or the border, Foreigners need to open a "Fideicomiso" to be able to by a property. This Fideocomiso got a fee.

Usually, the bank who will finance your property works with a "fiduciario", so please, do not start any process before getting your Pre-Approval to know the conditions of your future mortgage. We do not want you to have extra charges.

Prisma 67 is committed to transparency, and all fees will be clearly outlined during the application process. There are no hidden charges, and we ensure that you are fully informed of all costs involved. The bank pays us, not you.

How does Prisma 67 assist with the property purchasing process in Mexico ?

Prisma 67 provides comprehensive support throughout the property purchasing process:

Pre-Approval: We help you determine your budget and get pre-approved for a mortgage.

Property Search: We collaborate with reputable real estate agents and developers to help you find the perfect property.

Financing: We structure a mortgage that fits your financial situation and guide you through the entire financing process.

Closing: We work with legal professionals and notaries to ensure all documents are in order and the transaction is completed smoothly.

Post-Purchase Support: After your purchase, we offer ongoing support, including refinancing options and advice on property management

What happens if I need to sell my property before the mortgage is fully paid ?

If you decide to sell your property before your mortgage is fully paid off, Prisma 67 will assist you in managing the sale and settling the outstanding mortgage balance. We offer options such as refinancing or loan switching to help you manage your financial commitments effectively.

Our team will guide you through the process, ensuring that all legal and financial obligations are met.

It's possible to have some penalties for breaking your contract, but normally, after 48 months, you can liquidate your mortgage without any penalties.

We are a Financial Professional team fully certified and regulated by the “Asociación de Brokers Hipotecarios de México” At Prisma 67, your data and information are always safe.

Visit us on Social Medias

Email:

+1-450-485-6767

Office:

Calle 13 Sur, C. Diag. 70 Sur, Ejidal,

Playa del Carmen, Solidaridad,

Quintana Roo, Mexico

77712